Accelerate your path to financial freedom by being a live-in landlord

Take your wealth planning to the next level with my Wealth Planning Toolkit for Google Sheets – just $20.

Plan for recurring monthly income over different time periods as well as windfalls and one-time purchases in the future.

Includes 10 year Net Worth Tracker with Dashboard, Asset Rebalancing Calculator, and advanced FIRE and Coast FIRE Calculators.

What is House Hacking?

House hacking is where you purchase a single- or multi-family property and then live in the property while renting out a room or unit to help cover your mortgage expenses. The practice of house hacking is also known as being an owner-occupied landlord or live-in landlord. The key advantage to house hacking is that your tenants effectively help cover your mortgage payment which can reduce or even eliminate your housing expense. Since housing is the biggest monthly expense for most people, house hacking can help you to dial up your savings rate and reach financial independence sooner.

Advantages of House Hacking

- Being an owner occupant allows you to get the best financing terms. Generally, being an owner occupant allows you to get a lower interest rate than purchasing a property for investment purposes. If you choose to move out at some point and keep your property as a long-term rental, you can keep the owner-occupied loan in place.

- Smaller down payments are possible. Again, since you are purchasing the property with an owner-occupied loan, you are able to make a down payment as low as 0 to 5% the purchase price by using a VA loan or FHA loan. Loans for an investment property typically require a down payment of 20 to 25%.

- You likely only have to live there for one year. In general, the requirement for getting an owner-occupied loan is that you maintain occupancy for at least one year. This depends on the terms of your loan, so you should read the fine print before assuming the occupancy requirement. If you were to purchase a property with an owner-occupied loan and then did not live in the property for the first year, you would be committing mortgage fraud, which is a serious offense that can lead to fines and even prison time.

House Hacking approaches

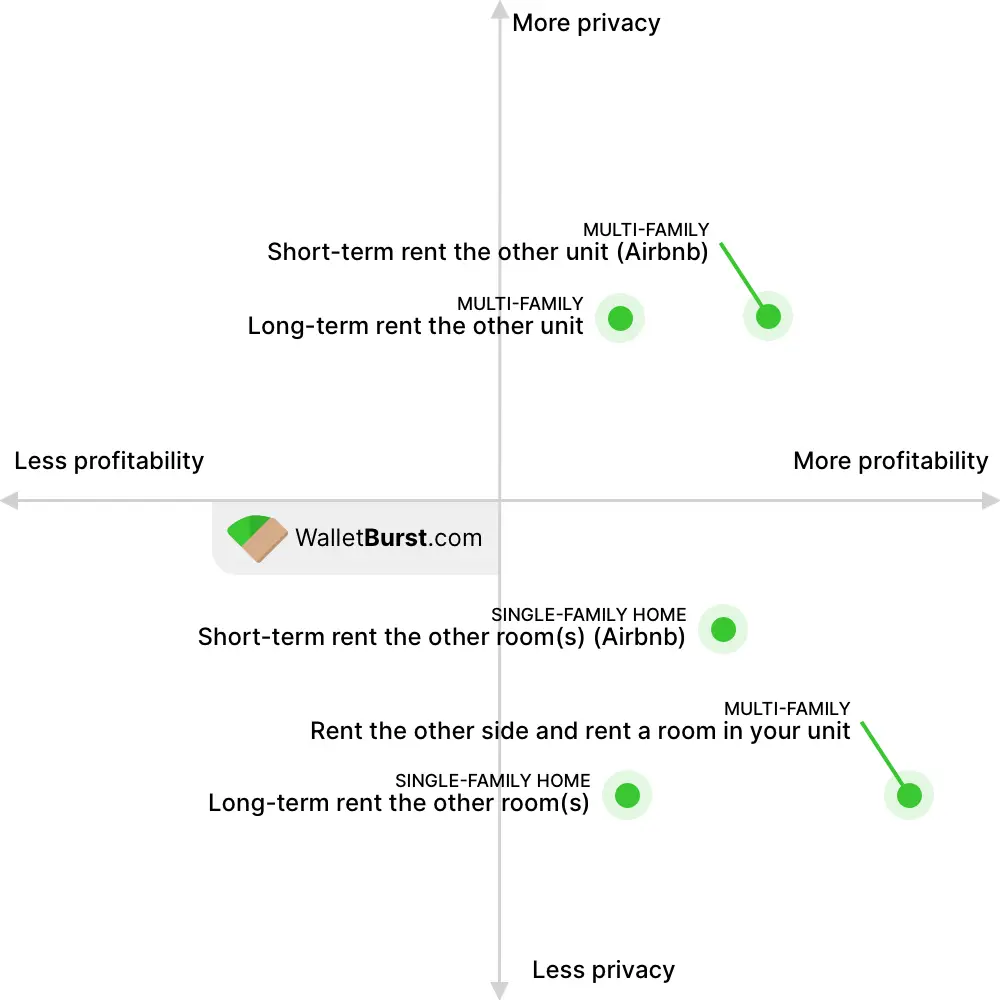

There is no one specific recipe for house hacking – it can be done successfully with several different types of properties. There are a wide variety of approaches that you can take depending on what kind of down payment you can afford and your comfort level with living with housemates. From a high level we can divide the strategies into two groups: Single-Family and Multi-Family. The 2×2 diagram below shows how the different strategies compare with respect to privacy and profitability.

Single Family Home

Compared to a multi-family property, a single-family home is generally going to have a lower purchase price which means you can start house-hacking with a lower down-payment. Single family homes are more widespread than multi-family properties, which can be quite rare to come on the market depending on your city. A common approach to house hacking with a single-family home is to rent out one or more of your extra bedrooms to housemates and share the common spaces. The drawback to this is that you sacrifice some of your privacy as you are effectively “living with roommates.” Make sure to check you local zoning laws as many cities limit the number of non-related people that can live in the same household. Strategies include:

- Long-term rent by the room. With this approach, you find long-term tenants for individual rooms in your house. By having your tenants sign a lease you can limit how often you need to fill vacant rooms.

- Short-term rent by the room (Airbnb). While similar to the approach above, renting out your rooms on a short-term basis offers the potential to make a bit more income and also the flexibility to have your place to yourself when you want. The downside is that being an Airbnb host requires time and effort and you would have more strangers coming and going.

In high cost of living areas like the SF Bay Area, Seattle, and Denver, house-hacking a single family home is popular because there is a large market of young people looking to rent by the room, and multi-family properties can be prohibitively expense.

Multi-Family

House-hacking with a multi-family property offers its own set of pros and cons. Low down payment loans like VA or FHA loans can be used to house-hack multi-family properties like duplexes, triplexes, fourplexes, or single-family homes with Accessory Dwelling Units (ADU). The drawbacks to the multi-family approach is that multi-family properties are more expensive (requiring a higher down-payment) and often harder to find on the market. On the plus side, multi-family house-hacking offers more privacy to you as the landlord and also offers the potential for more cashflow if you choose to move out and rent out all the units in the future. Strategies include:

- Long-term rent the other unit. The simplest multi-family approach is to live in one unit and rent out the other(s) to tenants on a long-term lease. Having long term leases gives you some predictability about vacancies, and is fairly hands-off aside from maintenance.

- Short-term rent the other unit (Airbnb). Since “entire places” command a premium on Airbnb, renting your other unit on a short-term basis can allow you to earn more each month than a long-term rental. The drawback is the time and effort required to be an Airbnb host.

- Rent the other unit and rent a room in your unit. The ultimate frugal house-hack is to both rent out the other unit (either short- or long-term) while at the same time renting out one of the rooms in your unit (also either short- or long-term). This may be the most profitable house-hacking strategy because it combines the rent-by-the-room model with the multi-family approach.

Overall House Hacking strategy

From a high-level, many real estate investors find house-hacking attractive because it allows them to accumulate a portfolio of rental properties with relatively low money down because of the benefits of owner-occupied loans that I previously mentioned. The common overall strategy for building wealth through house hacking is as follows:

- Buy your first house hack (HH#1).

- Live in HH#1 for at least one year while using the rent savings to help save up cash for another down payment.

- Buy your second house hack using this down payment (HH#2).

- Move out of HH#1 and place tenants to fully rent it out. With it fully rented, ideally it is providing a positive net cash flow.

- Live in HH#2 for at least one year. Use the rent savings from HH#2 and positive net cash flow from HH#1 to save up cash for another down payment.

- Repeat.

As you can see, this house-hacking strategy creates a snowball effect on your net worth where with each house hack you do, you create more positive cash flow. Even if you only want to do one house-hack and then get your own place, once you move out you can place tenants who will be helping to pay off your mortgage while your property also likely appreciates in value.

Craig Curelop is a golden example of this strategy executed to perfection. He started house-hacking in Denver, Colorado in 2017 and in just a few years, he was able to reach financial independence from the cash flow that his house hacks provided combined with the rapidly-appreciating Denver real estate market. To learn more about Craig’s strategy you can check out his book: The House Hacking Strategy: How to Use Your Home to Achieve Financial Freedom.

Drawbacks to House Hacking

While house hacking can be an amazing strategy with the right planning, it is not without its drawbacks:

- House hacking involves some sacrifice depending on which stage of life you are in. If you want to house-hack a single-family home, then you need to be comfortable with living with roommates. House-hacking a multi-family gives you more personal space as you can have the whole unit to yourself, but it still may be a step down in standard of living if you have a spouse and children and are used to living in a nice single family home.

- House hacking means becoming a landlord, and this brings with it several responsibilities. You have to stay on top of maintenance of your property, carefully vet tenants, and replace tenants when they move out.

- House-hacking does have some financial risks. While they are impossible to predict, black swan events like the Covid-19 pandemic can impact the ability of your tenants to pay rent, which could leave you on the hook for your mortgage payments with no rental income. Additionally, purchasing real estate with a low down payment means investing with high amounts of leverage. While leverage is great when prices are appreciating, it could also leave you owing more than the property is worth if your local market has a downturn.