Visualize and calculate how much you need to reach FI with a fat stash

Take your wealth planning to the next level with my Wealth Planning Toolkit for Google Sheets – just $20.

Plan for recurring monthly income over different time periods as well as windfalls and one-time purchases in the future.

Includes 10 year Net Worth Tracker with Dashboard, Asset Rebalancing Calculator, and advanced FIRE and Coast FIRE Calculators.

What is Fat FIRE (Financial Independence / Retire Early)?

If you’ve found your way to this Fat FIRE calculator, then you are likely already familiar with the concept of FIRE. Financial Independence / Retire Early (aka FIRE) is a personal finance milestone where you have accumulated enough assets that the returns on your investments are enough to cover your cost of living. Once you have reached FIRE, you can live off the returns from your investments indefinitely and have the freedom to spend your time however you like, without the need to work for income.

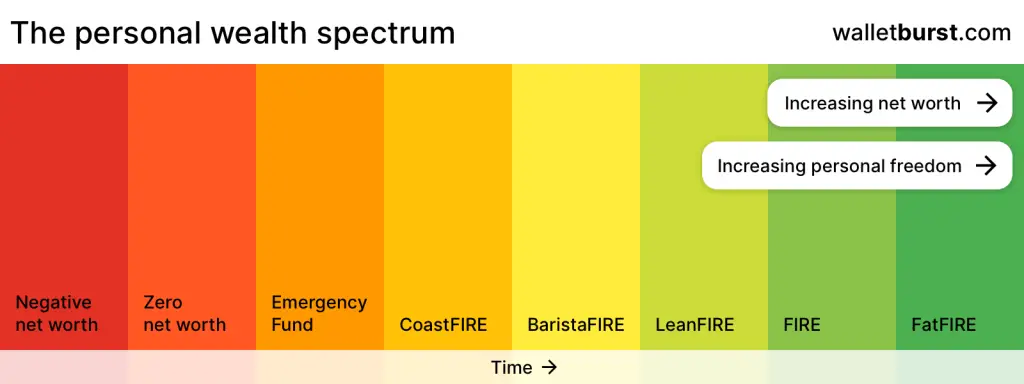

Fat FIRE is simply a variation of FIRE that entails having a “fatter” than normal nest egg which allows you to live life without sacrifices. As you can see in the personal wealth spectrum below, Fat FIRE takes the longest time to reach compared to other variations of FIRE, but also provides the most personal freedom.

While there is no fixed net worth number that defines the threshold from regular FIRE to Fat FIRE, I am going to put a stake in the ground and define Fat FIRE as having a high enough net worth to provide an income of $100,000 per year. Where do I get this number? Well, according to the US Bureau of Labor Statistics (BLS), the average US household spent somewhere between $50,000 and $60,000 on annual living expenses in 2019 not including pension or social security expenses. Fat FIRE is all about having a much better than average lifestyle in retirement, so let’s double $50,000 which gives us a nice round number of $100,000. The 4% rule implies that you would need to have $2.5 million in investments to provide $100k annually.

Let’s consider some of the other known FIRE milestones to make sure that this $100,000 number makes sense in context. Lean FIRE is generally defined as withdrawing less than $40,000 per year in retirement which means having an invested net worth of $1 million using the 4% rule. Then regular FIRE begins at a net worth of around $1MM and covers at least up to $2MM. Since Fat FIRE is by definition the opposite of Lean FIRE, then a starting net worth of about $2.5MM seems about right as the threshold for Fat FIRE, since it provides an annual income of 2.5x that of Lean FIRE.

Let me caveat the above by saying that the amount of income you need to live what you consider a “fat” lifestyle is going to vary heavily by individual factors like where you live, if you have a partner and/or kids, and what you consider to be your baseline standard of living. A lifestyle of minimal financial sacrifice is going to require a much higher net worth if you have a family in the San Francisco Bay Area than if you are a bachelor living in the midwest. Fat FIRE is a very subjective milestone that only you can determine for yourself.

How do I calculate my Fat FIRE number?

Your Fat FIRE number is the amount of money you need to have invested such that the returns from your investments are enough to cover your ongoing living expenses. This number is based only on your estimated annual spending in retirement and your Safe Withdrawal Rate (SWR):

(Fat FIRE number) = (annual spending) / SWRSafe Withdrawal Rate (SWR) is the estimated percentage of your net worth that you expect to withdraw to cover your living expenses in retirement. 4% is widely considered as the recommended SWR for retirement planning. This 4% withdrawal rate was found by the Trinity Study to have a 100% success rate over a 30-year retirement horizon with a 50% / 50% mix of stocks and bonds.

Using this calculator

This interactive calculator makes it easy to calculate and visualize the growth of your net worth on your journey to Fat FIRE.

To use this calculator, simply fill in the inputs at the top of the page and watch the graph automatically update!

- Start by entering your current age, current annual take-home pay, and current annual spending. Your current annual take-home pay is your post-tax income and does include any contributions that you make to retirement accounts like a 401k or HSA.

- Annual spending in retirement is the amount you plan to spend each year in retirement. Note that in many cases, this number will be less your current spending, because (1) you will be covered by Medicare and (2) you may have paid off your primary residence, so you no longer have to pay a mortgage.

- Current Net Worth is your total current net worth including stocks, bonds, cash, and retirement accounts. This would not include real estate equity, unless you later plan to sell your real estate in retirement. For example, if you have $100,000 invested in the stock market (perhaps through your employer’s 401k) and $25,000 saved in your emergency fund, then you should enter $125,000 in this field.

- Use the sliders to adjust the rates and watch the graph to the right immediately react to your change!

- Investment rate of return is the average return that you expect your investments to grow, not adjusted for inflation. This calculator uses 7% as a default Investment rate of return, which is a relatively conservative assumption. Historically, the S&P 500 has returned on average 10% annually from its inception in 1926 to 2018.

- Inflation rate is the average annual rate of inflation that you expect to experience in the future. Historically, the US economy has experienced an annual average inflation rate of 3%.

- Safe Withdrawal Rate (SWR) is the estimated percentage of your net worth that you expect to withdraw to cover your living expenses in retirement. 4% is widely considered as the recommended SWR for retirement planning. This 4% withdrawal rate was found by the Trinity Study to have a 100% success rate over a 30-year retirement horizon with a 50% / 50% mix of stocks and bonds.

The math behind the calculator

This calculator uses your input allocation percentages and rate-of-return for each to calculate a weighted-average rate-of-return for your net worth as it moves through the simulation.

At its core, this calculator uses the compound interest formula:

A = P * ( 1 + n)^tHere A is the final amount, P is the principle (initial amount), n is the annual growth rate, and t is the time in years.

Your net worth is calculated recursively (based off the previous year) on a year by year basis, starting at the present day (year 0) with your given inputs. For example:

Net worth at year 1 = previousYearNetWorth * (1 + rate) + (startingTakeHomePay - startingAnnualSpending) + (startingSalary * company401kmatch)Here rate is your weighted-average rate-of-return minus the inflation rate. In this case, previousYearNetWorth is your starting net worth. In subsequent years, startingTakeHomePay and startingSalary are increased using the compound interest formula with the income growth rate that you input.

What about inflation?

Inflation is an important variable to account for when planning for retirement decades in the future. It is almost certain that we will experience inflation in the future, and for this reason having your money invested in assets and not all stuffed under your mattress is crucially important. Assets like stocks and real estate tend to rise with inflation while cash loses value, meaning the best way to preserve your wealth in times of high inflation is to be invested in these assets.

Don’t worry about inflation, it’s built-in to the calculator! This calculator accounts for inflation by subtracting the inflation rate (from the input slider) from the investment growth rate of return. This gives an inflation-adjusted rate of return which is then used to calculate your Fat FIRE number and draw the graph. With this approach, all the numbers in the calculator are adjusted to be in 2020 dollars. Think about it like this – you don’t have to worry about cost-of-living increases because it’s already skimmed off of your expected investment returns.