What is Coast FIRE?

Put simply, Coast FIRE is when you have enough in your retirement accounts that without any additional contributions, your net worth will grow to support retirement at a traditional retirement age.

After your net worth has passed what we will call your Coast FIRE number, you still need to earn enough to cover your expenses each month, but you no longer need to be saving to ensure your traditional retirement. Using historically proven growth and inflation rates, you can allow the compounding growth of your existing investments over time do the heavy lifting for you. This means that you gain the freedom to pursue a different job that pays less, shift to working part-time, or just have more spending money to enjoy life.

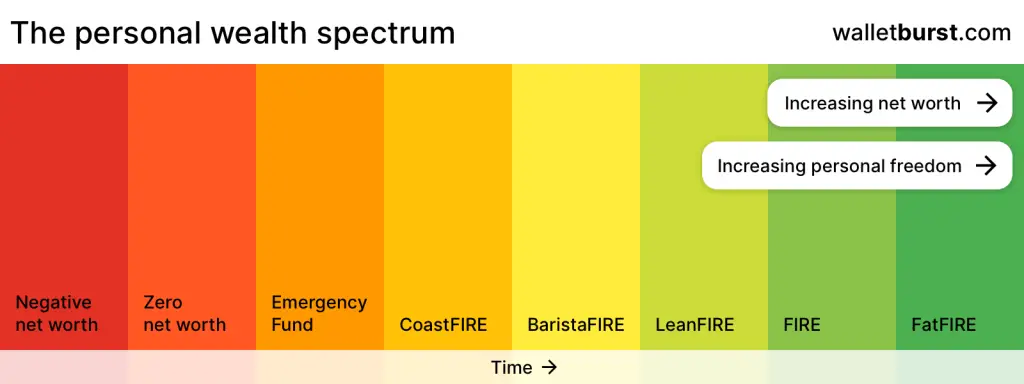

Personal wealth is a Spectrum

Before we get into the concept of Coast FIRE, let’s take a step back for a moment and look at what I call the personal wealth spectrum. If you’ve spent some time reading about Financial Independence, you’ve likely come across the many variations of FIRE. There’s LeanFIRE, FatFIRE, BaristaFIRE, SlowFIRE, Coast FIRE and even Flamingo FIRE. The list goes on and on, but don’t let these labels confuse you. A helpful way to make sense of these variations is to think about different personal wealth milestones as being along a spectrum, with each of these variations of FIRE just a different point along that spectrum.

Coast FIRE is a particularly interesting milestone along the personal wealth spectrum because of the freedom that it unlocks and how achievable it is to get to this point compared to regular FIRE.

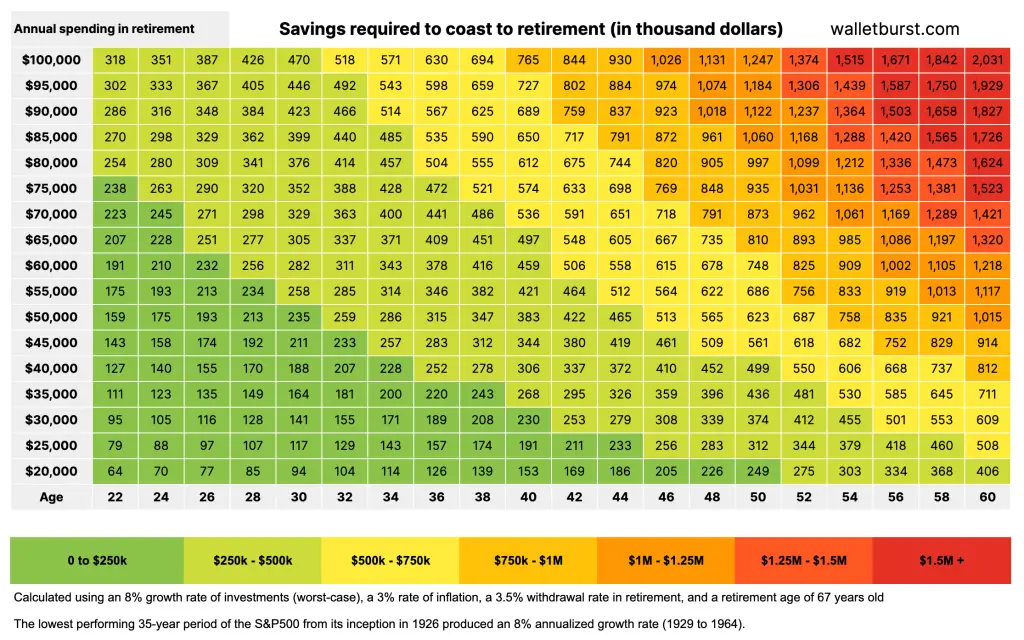

By working backwards from a traditional retirement age, Coast FIRE takes advantage of the power of compounding more than other variations of FIRE. This means that the younger you are, the lower your Coast FIRE number because you have more time for your net worth to grow. In fact, with modest spending needs in retirement, Coast FIRE is remarkably achievable for money savvy 20- and 30- somethings. The lookup grid below makes it easy to see how age and spending in retirement can impact your Coast FIRE number.

Although the stock market has historically produced an annualized average return of about 10% over the last century (source: MarketWatch), I used an 8% annual return for the grid to illustrate the historical worst-case scenario. Since its inception in 1926, the S&P500 index’s lowest-performing 35-year period produced an annualized return of 8% from 1929 to 1964 (source: A Wealth of Common Sense). Even if you invested a lump sum at the peak of the market in 1929, right before the biggest crash in stock market history, you would have still experienced an 8% annualized return if you stayed in the market for the next 35 years.

Note that the expected spending in retirement numbers in the grid are in today’s dollars, meaning that you do not need to account for inflation since it is already baked in to the graph. For more details about the grid, you can read my article: The Coast FIRE Grid: how much do you need to save up to coast to retirement?

How do I calculate my Coast FIRE number?

I built a Coast FIRE Calculator to allow you to easily calculate your Coast Fire number and visualize your Coast FIRE path.

(This section is going to get into the mathy bits of calculating your Coast FIRE number. You can skip ahead to the Coast FIRE number example calculation section to see it in action.)

First, let’s recall how to calculate your regular FIRE number:

(FIRE number) = (annual spending) / SWRHere, the SWR (safe withdrawal rate) is the percentage you can withdraw from your portfolio each year without reducing your principle. In theory, each year you could withdraw this percentage from your portfolio indefinitely because you are not touching the principle. Based on the Trinity study, a SWR of 3 to 4% is recommended depending on your age and risk tolerance. For calculating our Coast FIRE number, this FIRE number above is the amount we wish to have at our traditional retirement age.

Next we will consider the compound interest formula that you probably learned in middle school:

A = P * ( 1 + n)^tHere A is the final amount, P is the principle (initial amount), n is the annual growth rate, and t is the time in years. We can set our final amount A to be equal to our FIRE number and then solve for P, the initial amount, which is our Coast FIRE number. This gives us:

(Coast FIRE number) = (annual spending) / ( SWR * (1 + n)^t )Now we can see that your Coast FIRE number will depend on your annual spending in retirement, your safe withdrawal rate once you hit retirement, the net growth rate of your investments (n) and the time period (t) between the age when you hit your Coast FIRE number and your retirement age. To account for inflation and keep all the numbers adjusted to the current year, the net growth rate (n) should equal the expected rate of return (r) of your investments minus the expected rate of inflation. Thus n = r – i.

Notice how in the above formula, the time t is the exponent? This explains why saving and investing at an earlier age has an exponential effect on increasing your wealth. This is crucially important for Coast FIRE, because the younger you are, the more time for your net worth to grow and the less money you need to have invested.

Coast FIRE number example calculation

To help make sense of these numbers, let’s do an example with a guy named Cal. Cal is 30 years old and is planning to need $40,000 per year to live on in retirement. How much does Cal need to have invested at his age to Coast FIRE?

First, let’s make some conservative assumptions since Cal is a long ways from traditional retirement:

- An average investment rate of return (r) of 7%

- An average inflation rate (i) of 3%

- A safe withdrawal rate (SWR) of 3.5%

Also, we’ll assume that Cal will retire at age 67, which is considered the standard retirement age. Remember that n = r – i = 0.07 – 0.03 = 0.04

Now we just have to plug these numbers into a calculator:

(Coast FIRE number) = (40,000) / (0.035 * (1 + 0.04)^(67-30) ) = $267,768If Cal wants to downshift into Coast FIRE at his current age of 30, he needs to have $267,768 invested given his relatively conservative strategy. While over a quarter million is no small chunk of change, Cal could realistically get there by maxing out his 401k each year starting at age 21 with no savings.

The importance of saving and investing at a young age

To understand the importance of saving earlier in life, let’s revisit our previous example and see what happens to Cal if he waits until his 30s to start saving. If he wants to start coasting at age 40 with the same annual spending in retirement, a quick glance at the lookup table shows that he needs to have about $396k invested. Saving up nearly $400k from age 30 to 40 is likely going to be more difficult than $270k from age 20 to 30, especially considering that Cal is more likely to settle down and start a family after age 30.

Why I think Coast FIRE is so awesome

When I first heard of Coast FIRE and realized that I had already passed my Coast FIRE milestone ( albeit with some portfolio rebalancing), I got pretty excited. Although I still have a ways to go before hitting my actual FIRE number, knowing that I’m already set for traditional retirement without contributing any more for the rest of my life feels tremendously freeing.

Here’s a few of the other benefits that I feel make Coast FIRE a special personal wealth milestone:

- You gain a ton of options for how you make money now that you only need to cover your living expenses going forward.

- You have peace of mind knowing that your retirement is secured based on historical rates of growth and inflation.

- As you continue past your Coast FIRE milestone, any additional retirement savings you make will “bring in” the point that you reach FIRE to a nearer date.

What could your Coast FIRE life look like?

When you only need to make enough money to cover your living expenses while still having a secured retirement, the options really open up for your lifestyle and career. Here are a few approaches you could take to increase your freedom and improve your quality of life when you reach your Coast FIRE milestone:

- You could continue in your current career in a part-time capacity, like consulting.

- You could change careers to something that you’re more passionate about, gives you more meaning, or is lower stress.

- You could do flexible gig economy work like Uber, Amazon Flex, Instacart or TaskRabbit.

- You could start a small business, like being an airbnb host, lawn care, or petsitting.

- You could work in an outdoors setting in a National Park, at a ski resort, or as a tour guide.

The options really are endless, and it’s worth thinking about what kind of job you would enjoy if money was no object.

Most early retirees realize that even after they retire, they still need something to do with their time and to give meaning to their life. You don’t need to wait until you’re fully financially independent to experience freedom and find more meaning and enjoyment in your life. This is why Coast FIRE is such a special personal wealth milestone.

Feel free to share in the comments below. I’d love to hear what your Coast FIRE number is and how you plan to change your life once you reach your Coast FIRE milestone.