Use this simple calculator to determine your personal savings rate (ratio) for FIRE

Take your wealth planning to the next level with my Wealth Planning Toolkit for Google Sheets – just $20.

Plan for recurring monthly income over different time periods as well as windfalls and one-time purchases in the future.

Includes 10 year Net Worth Tracker with Dashboard, Asset Rebalancing Calculator, and advanced FIRE and Coast FIRE Calculators.

What is my Savings Rate / Savings Ratio?

Your personal savings rate, (or savings ratio) is a measure of how much of your personal disposable income is saved rather than spent. It is the ratio of your personal savings divided by disposable income over a given period and is typically written as a percentage. Your disposable income should be used to calculate savings rate and this is your total income after all income taxes.

The higher your savings rate, the stronger your personal financial situation. A savings rate of 0% means that you spend all of your income and save none of your income. On the other hand, a savings rate of 100% means that you save all of your income and spend none of your income.

How do I calculate my Savings Rate?

Savings Rate (SR) is defined as the ratio of savings divided by your income. Your savings over any period is your income – expenses. Thus your SR = (Income after tax – spending) / (Income after tax). To convert this SR to a percentage, multiply by 100.

Using this calculator

This interactive calculator makes it easy to calculate and visualize your personal savings rate. Simply input your monthly take-home pay and monthly spending.

What is a good savings rate?

As a rule, the higher your savings rate, the faster that you can achieve financial independence. What is a “good” savings rate depends highly on your individual situation and how much you are able to save. At a minimum, you should aim to have a savings rate of 20%. While you should strive to maintain as high a savings rate as possible, you should still allow yourself to spend enough to enjoy life. According to the Federal Reserve Bank of St Louis, the personal savings rate across the USA was about 14.3% as of September 2020.

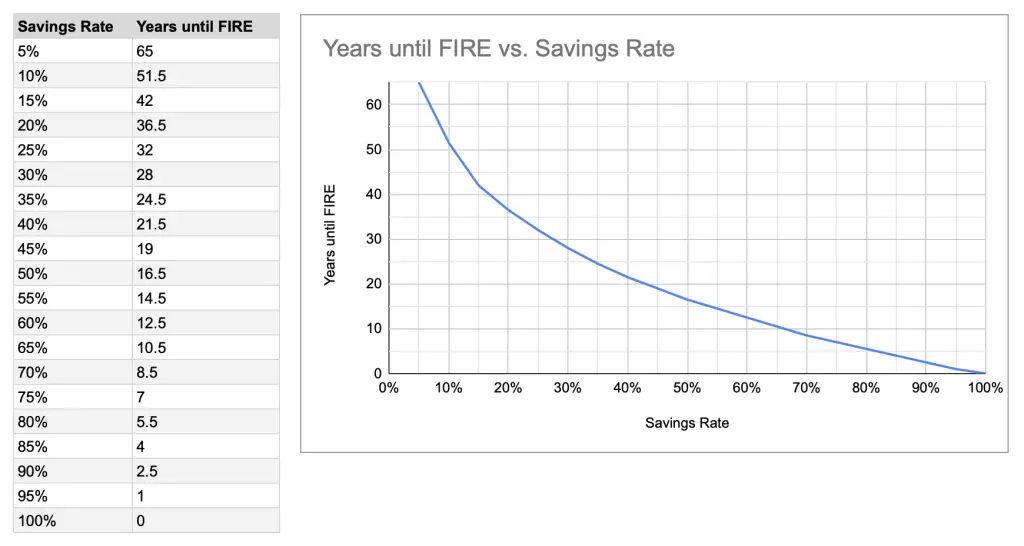

Savings rate and time to financial independence (FIRE)

Regardless of how high your income or your expenses, your savings rate alone determines how soon you can reach FIRE. Mr. Money Mustache detailed this concept in his infamous article, The Shockingly Simple Math Behind Early Retirement. If your savings rate is 0%, then you will never save up enough to retire, as you are spending 100% of your income. Conversely, if your savings rate is 100%, then you spend none of your income and you would be considered Financially Independent (FI).

The table and graph below illustrate the relationship between savings rate and time to FI. To generate these numbers, I used the WalletBurst FIRE Calculator with a starting net worth of $0, a 100% allocation into stocks, an 8% rate of return, and 3% inflation rate. Looking at the graph, it’s interesting to note that the curve is not linear but rather exponential. The curve is steepest from 0% to about a 25% savings rate, and beyond a 25% savings rate, it becomes roughly linear. The big takeaway from the graph is that the biggest improvements to time-to-FIRE are at lower savings rates. Increasing your savings rate from 10% to 20% speeds up your time-to-FIRE by 15 years, while going from 50% to 60% only gets you 4 years closer to FIRE.