When it comes to accelerating your path to financial independence, one of the most important metrics to control is your personal savings rate. No matter how high your income is, your savings rate alone determines how quickly you can reach financial independence. As a rule, the higher your savings rate, the faster that you can achieve financial independence. What is a “good” savings rate depends highly on your individual situation and how much you are able to save. To learn more about savings rate and to calculate your own personal savings rate, check out my simple Savings Rate Calculator.

Here is a breakdown of how I maintain a savings rate of over 65% while living in the Very High Cost of Living (VHCOL) San Francisco Bay Area with a fairly average salary for the region.

Expenses

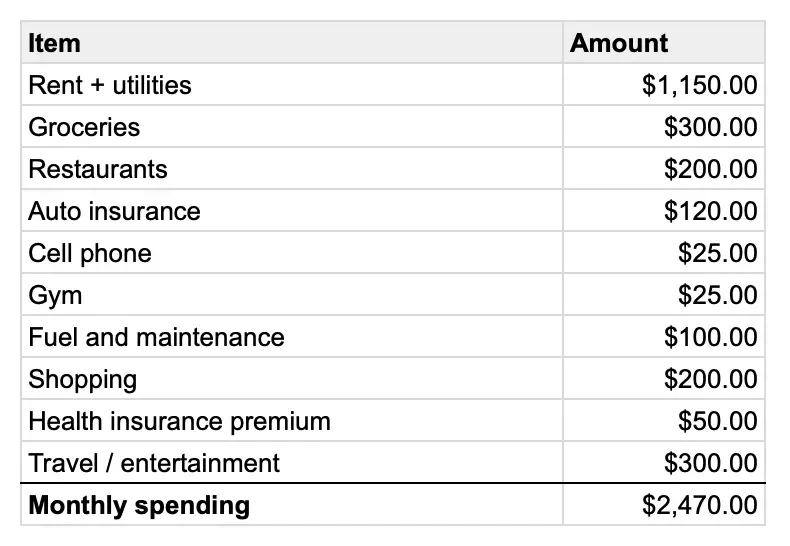

Overall, my expenses work out to roughly $2,500 per month, which I consider to be pretty good for someone with their own place in the SF bay area. While I am certainly not getting bottle service every weekend on this budget, I honestly don’t feel like I’m missing out on much. I have my own place, enjoy going out to bars or restaurants on weekends with buddies/dates, fly home to the midwest a few times a year, and enjoy an international trip every year.

My real secret to living on $30k per year in the VHCOL SF bay area is that I found a great deal on an unconventional studio setup. I pay $1,150 per month for a small studio that is above my landlord’s garage in Mountain View, CA. I have my own entrance, my own restroom, and a small kitchenette with fridge, sink, induction stove, microwave, etc. It’s not good for cooking or entertaining large groups, but it’s great for 1-2 people and is the perfect setup for where I’m at in life. When you consider that my rent includes all utilities, I am basically paying the going rate for a single room in a house in the bay area, but instead I get my own little studio.

Below is a complete look at my monthly expenses. Keep in mind that my spending categories tend to fluctuate month-to-month but overall they balance out:

Income

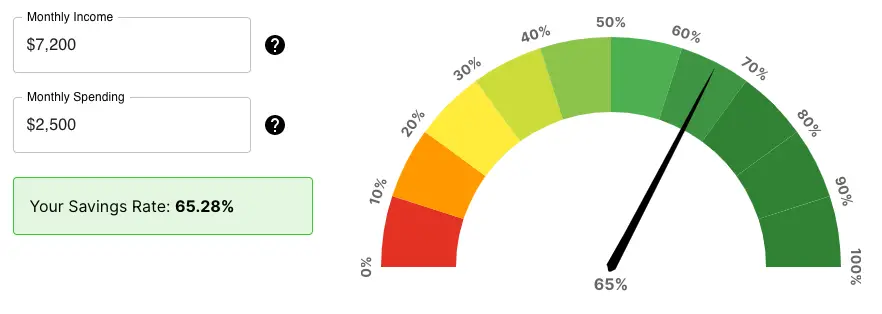

My base salary as a mechanical design engineer is $115k, which is pretty average for someone with my level of experience in the bay area. Using the SmartAsset Income tax calculator, my annual take home pay works out to about $86,500 per year or $7200 per month. Note that I also have a stock option component to my compensation, but I will keep this out of the calculation as this value is subject to stock market turbulence.

Savings Rate

Plugging my monthly income and spending into my Savings Rate Calculator, I calculate a savings rate of about 65%, which is pretty decent. Even if I was starting with zero net worth, this 65% savings rate would enable me to hit my FIRE milestone in just 10.5 years!

Advice: Focus on the big three

There are two real levers that you can pull in order to increase your savings rate: boosting your income and reducing your expenses. Reducing your expenses is a great place to start, but it can only take you so far as everyone needs to maintain a basic standard of living.

To reduce your expenses, focus on optimizing your big three expense categories: housing, food, and transportation. The average US household spends about 48% of their income on these three areas.

Since rent and utilities is the biggest monthly expense for most people, this is really the area of your budget where you can make the biggest impact on your savings rate. Some strategies to keep your housing expenses in check include:

- Living with roommates

- House hacking (check out my house hacking calculator)

- Renting out a spare bedroom on Airbnb

- Downsizing your house

- Finding a “unique” setup like my studio mentioned above

After housing, food expenses are typically the next largest spending category in most people’s monthly budget. Here are some things you can do to save on food while keeping your sanity:

- Instead of going out for lunch every day at work, do a “meal prep” on the weekend so that you have lunch pre-made each day of the week. I’ve been doing this for the last four years and it quickly becomes a habit. The key is to mix things up to keep it interesting and prep base foods like meats, rice, and veggies that you can combine in different ways to make a variety of dishes throughout the week.

- Shop at discount grocery stores. Rather than filling up your cart at Whole Foods every week, check out discount grocery stores like Aldi, Grocery Outlet, WinCo, or HEB.

- Make going out to eat at restaurants a special occasion instead of an everyday habit. The more you eat out, the less “special” it feels.

Lastly, to reduce your transportation costs, it comes down to not driving more than you can afford. When possible, avoid financing a vehicle purchase, because if you have to finance it, you probably can’t afford it. For most people, a $10k used sedan will get the job done for many years to come.