Your choice: $500 per month or $100k upfront?

Let me make you a hypothetical offer. Which would you rather have, $500 of pure passive income that you receive every month in perpetuity (that grows with inflation), or a one-time grant of $100,000 in a total stock market index fund today? While $100k upfront is enticing and you could likely leverage it to start a business or make a real estate investment, as far as pure passive income goes, the inflation-adjusted $500 per month is actually worth much more than $100k. If you cheated and looked at the SWR Passive Income Grid above, you might have chosen the $500. To understand why the $500 per month is likely worth more than $100k upfront, let’s review the idea of Safe Withdrawal Rate and the 4% rule.

What is Safe Withdrawal Rate (SWR)?

Simply put, Safe Withdrawal Rate (SWR) is the rate at which you can plan to earn passive income from invested assets while having a high likelihood of preserving your initial investment over the long term.

In this grid and in this article, “invested assets” refers to broad-based stock market index funds like VTI, VTSAX, or VTSMX which track the total stock market. This is the rate at which you can “safely” withdraw the returns from an investment without tapping into your principle, hence the name Safe Withdrawal Rate. Here’s the formula:

SWR = annual portfolio withdrawal / portfolio valueIn the financial independence and retirement planning world, the term SWR is often associated with the 4% Rule. The often-quoted 4% Rule is simply the idea that you can use a SWR of 4% when calculating your required nest egg to plan for retirement. The value of 4% is based on the infamous Trinity study, where researchers backtested historical stock market data and found that using a 4% investment withdrawal rate had an extremely low probability of exhausting a portfolio over any 30 year period. This 4% SWR takes into account historical market appreciation as well as inflation, so when using the 4% rule you can think in terms of today’s dollars.

For a retirement period of over 30 years, you may want to consider reducing your SWR to improve your portfolio’s chances of success. An easy way to think about SWR is that the higher the SWR, the more risky your retirement strategy but also the less investment you need for a desired passive income. If you only need your portfolio to last 10 years, then you could plan for a higher SWR than if you need your portfolio to last 40 years.

Back to our example…

Let’s view our example of $500 passive income per month versus $100k upfront through the lens of the 4% rule. A quick rule of thumb with the 4% rule is to take the annual investment withdrawal and multiply it by 25 (the same as dividing by 4%).

$500 per month * 12 months = $6,000 per year. Using the formula SWR = annual portfolio withdrawal / portfolio value, and rearranging, our required portfolio value = $6,000 / ( 4/100 ) = $6,000 * 25 = $150,000. If we’re planning beyond 30 years and want to reduce our SWR a bit to say 3%, then our required portfolio value becomes a whopping $200,000 to yield $500 per month using the 4% rule.

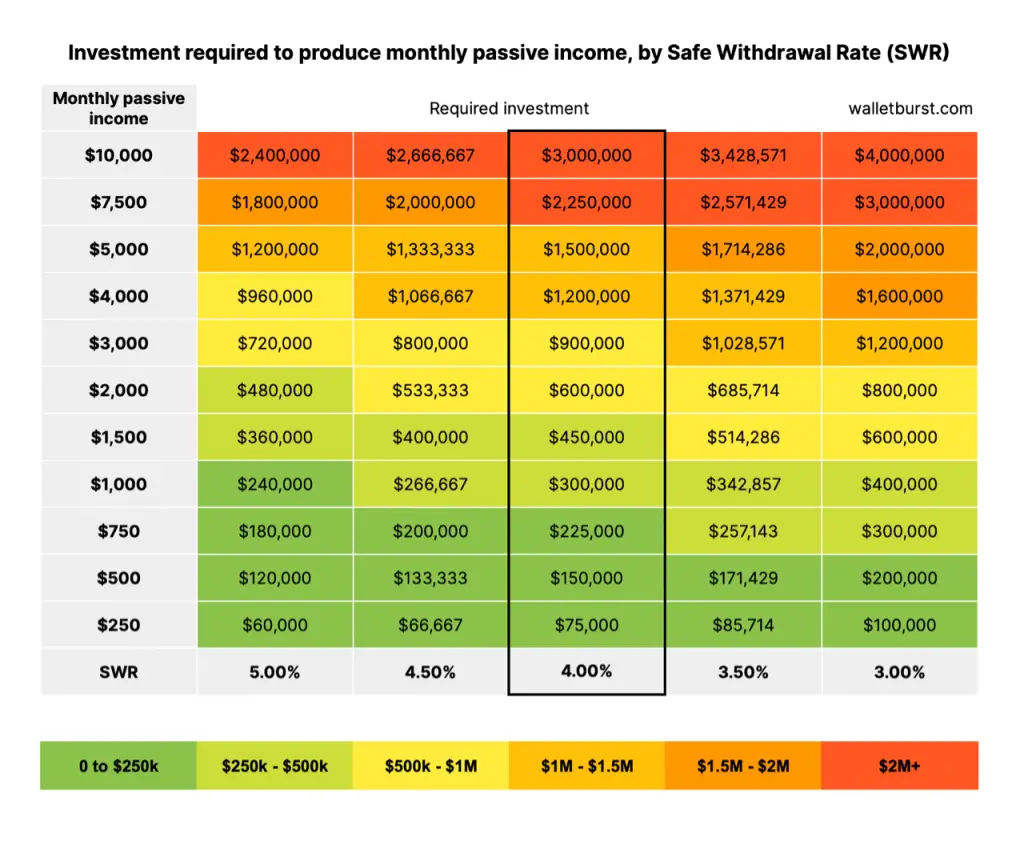

The Passive Income Grid

To save you from doing the math, I made this passive income grid to help you visualize the amount of invested assets you need to generate a desired monthly passive income at various Safe Withdrawal Rates (SWR). With your average monthly spending (pre-tax) and target SWR (based on your risk appetite) in mind, you can quickly look up on the grid how much invested assets you need to be financially independent (FIRE).

The value of passive income

The grid highlights just how valuable passive income is towards reducing your net worth required to reach financial independence. For example, earning just $1,000 per month of passive income is worth $300k in invested assets, which could take you several years to accumulate. You can dramatically accelerate your path to financial freedom by building passive income streams. Some examples include selling digital products, building high-traffic websites, or investing in real estate where you outsource the day-to-day management. These income streams all entail using some kind of leverage (like a mortgage or the near zero marginal cost of software code) to earn the same amount of passive income with much less initial investment.