👋 Hey there, welcome to the WalletBurst monthly newsletter for the month of April 2022.

Around the web

🧐 With inflation being top of mind lately, I really enjoyed Nick Maggiulli’s article titled You’ve Been Thinking About Inflation All Wrong. Nick makes the point that keeping up with inflation is much more nuanced than simply getting a raise that is equal to the Consumer Price Index (CPI). If you are a heavy saver, then you need less of a raise to cover an increase in spending than a person who is living paycheck-to-paycheck, which makes sense.

However in his article, Nick does not consider 1) the impact of income taxes on how much of a raise is required, and 2) the fact that just getting enough of a raise to cover your increased spending will diminish your savings rate over time. #2 is super important because your savings rate is the single factor that determines your timeline to financial independence.

To expand on Nick’s concept, I built a Keeping Up With Inflation Calculator which calculates how much of a raise you need to keep up with inflation and adds these additional factors of marginal income tax rate and maintaining the same savings rate that you had initially.

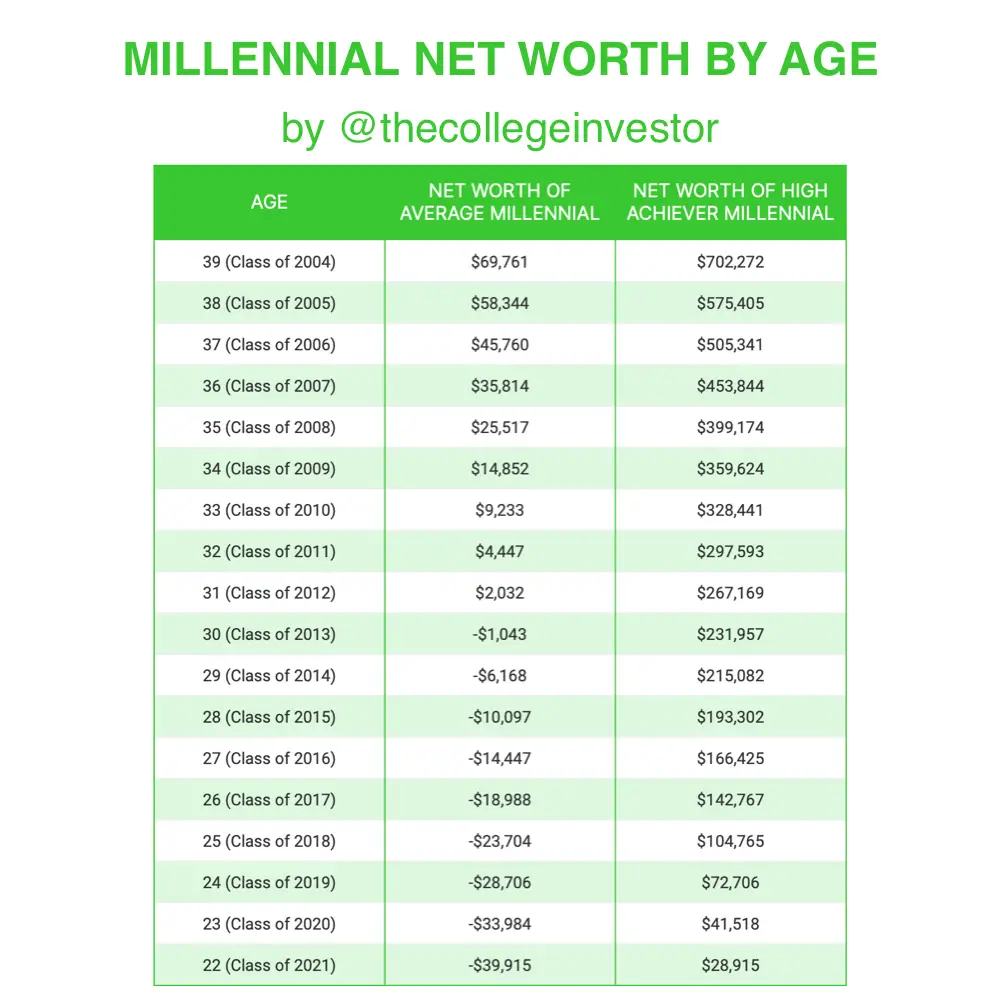

🥑 I know comparison is the thief of joy and all, but I think benchmarking your net worth against your peers is a good to way to get some perspective on your progress and appreciate how you are doing in this age of fake wealth on social media, which is apparently now a whole industry. Anyways, in his piece titled The Average Net Worth Of Millennials By Age, The College Investor put together net worth numbers for average and high-achieving millennials based on data from the Federal Reserve. While I feel like these numbers are a bit low, his methodology makes a lot of since when considering stats from the federal reserve and average student loan debts. I put together this table with the data at-a-glance, but check out his full article for details on how Robert put together the net worth benchmarks.

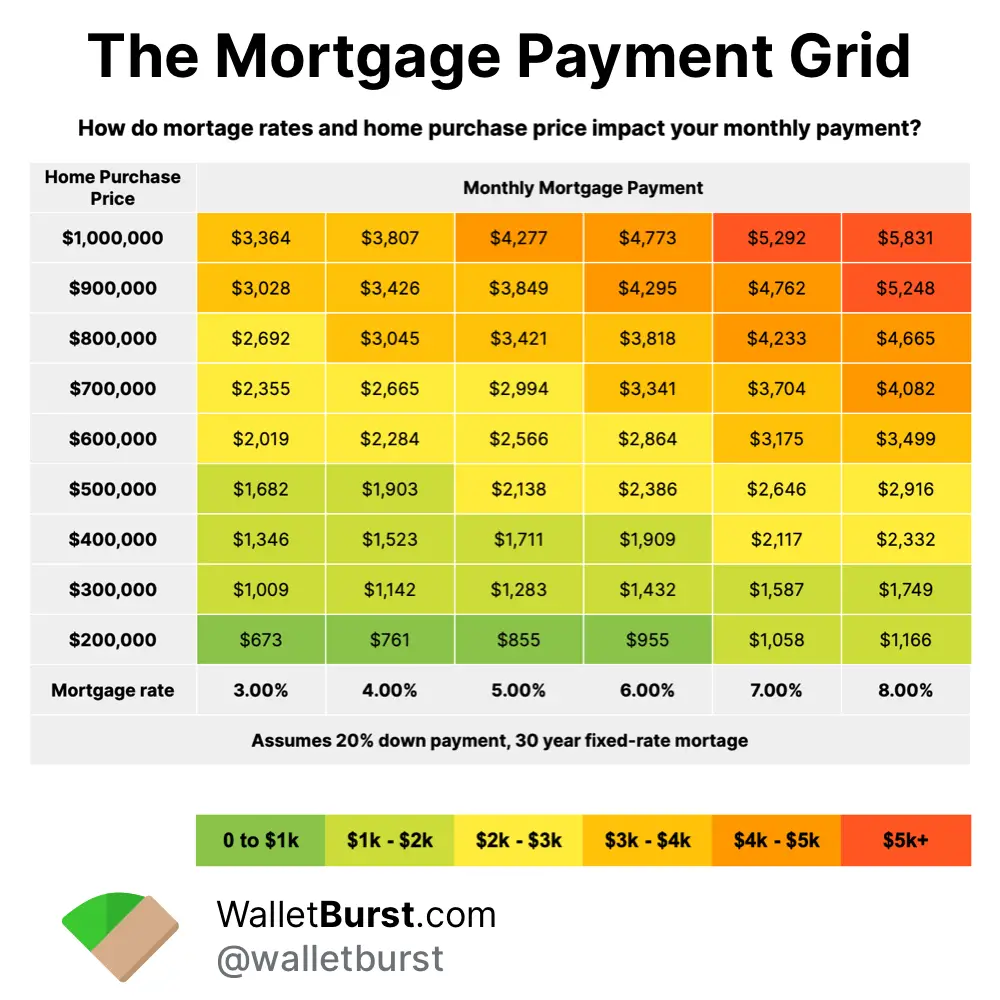

🏠 In the last few months, we have seen mortgage interest rates experience the sharpest rise in the last 30 years. What this will mean for the housing market is uncertain, but its interesting to consider just how much rising mortgage rates impact home affordability. I made this grid shown below to show how mortgage rates impact the the monthly mortgage payment for different home purchase prices. These numbers assume a 30 year fixed-rate mortgage and a 20% down payment. Consider that in late 2021, mortgage rates on a 30 year fixed loan were still around 3%, and now in April 2022, they are reaching close to 6%, with higher rates on the horizon. If we see rates get up to 7%, that will mean a roughly 50% increase in monthly payment, in a matter of months. Given all the other inflationary pressures on consumers, one has to wonder what kind of impact this rise in rates will have on home prices.

New on WalletBurst.com

End Note

Thanks for reading! If you’re enjoying my newsletter, I’d love it if you shared it with a friend or two. You can send them here to sign up.

And if you have any feedback on my site or come across any interesting personal finance content, send it my way to andrew@walletburst.com. I love to hear from my readers/users!

Have a great day,

Andrew ✌️