Inflation in the spotlight

If we had to pick one word to sum up what happened in the financial world in 2021, it would probably be inflation.

Inflation has been all over the headlines recently as the annualized CPI (Consumer Price Index) inflation rate reached 7% in December of 2021, the highest since June of 1982. And this 7% CPI number pales in comparison with the over 18% growth of home prices over the past year. Since the pandemic began in 2020, cost of living has increased across the board at a much faster pace than in recent history.

While the Financial Independence / Retire Early (FIRE) movement picked up steam over the last decade, we were in a period of relatively low inflation, along with strong growth in the stock market. Inflation wasn’t much of a concern, and it was easy to just assume a 3% annual inflation rate based off of historical averages. But with inflation now surging as the Federal Reserve has rapidly expanded the money supply in the last two years, building an inflation-proof financial plan is absolutely critical if you’re planning on retiring early, or even retiring at all.

Note that this article is tailored more towards the lean to traditional FIRE crowd aiming to escape the 9 to 5 earlier in life.

In this article we’ll consider how you can position both your expenses and your investments to maintain your standard of living while inflation tries to eat away at it.

First let’s consider how inflation impacts your expenses.

Where does inflation hit your budget the hardest?

To understand how to combat inflation in your early retirement plan, let’s focus on the overlap between:

- The largest line items on your monthly budget.

- The spending areas that have historically been most prone to inflation.

Using data from the Bureau of Labor Statistics, these are typically the largest spending categories:

- Housing

- Transportation

- Healthcare

- Food

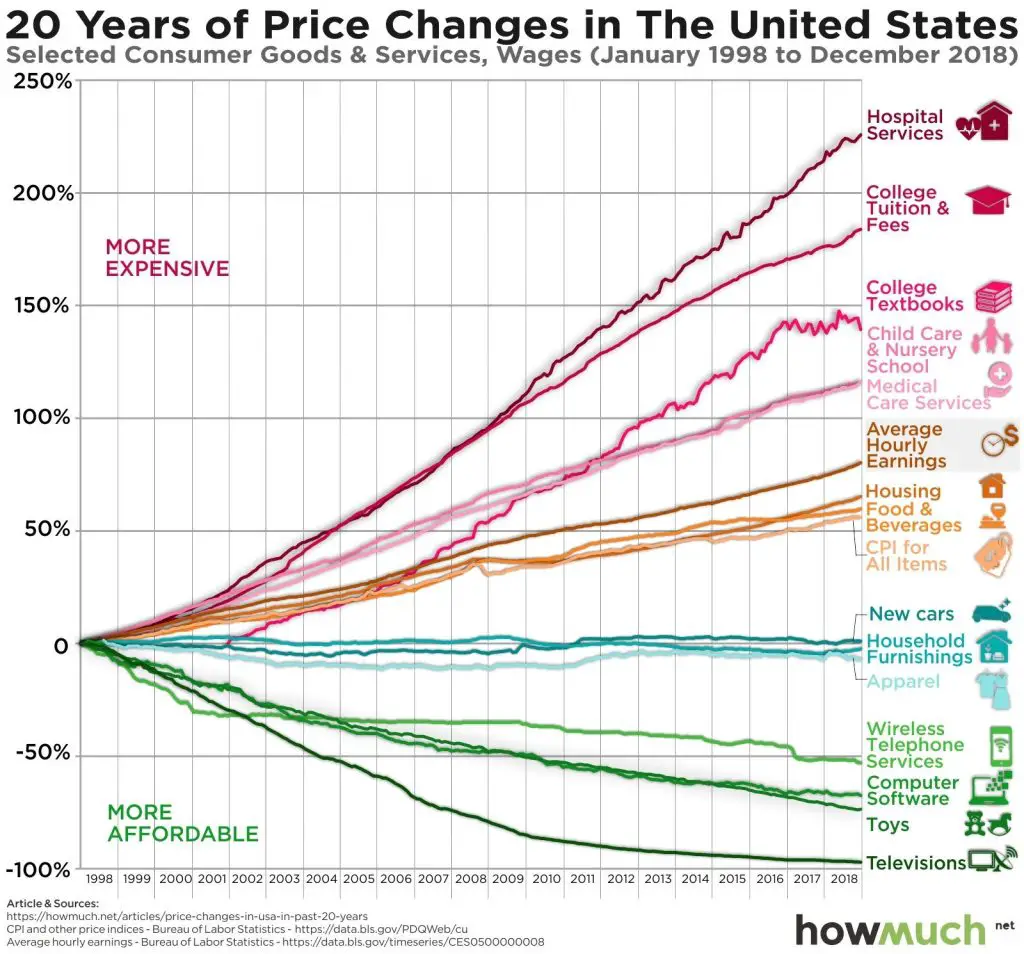

Now let’s consider the categories that have been most impacted by inflation over the last 20 years with this graphic courtesy of howmuch.net.

Here, the following categories have increased the most in price over the last 20 years:

- Hospital services

- College tuition and textbooks

- Child care

- Medical care services

- Housing

The graphic shows that unfortunately, the things that are most important to quality of life like healthcare, education, and housing have experienced the most inflation. On the positive side, some of these categories like child care are likely not relevant to your retirement plan, so we don’t have to worry about them. Food costs have roughly tracked CPI over the last 20 years, and vehicles have stayed fairly flat. Plus, with no job to commute to, there is a good chance that your transportation costs may be lower in retirement and a smaller proportion of your budget.

Overlapping these two lists, we can see that housing, health care, and potentially also college education are the categories that we need to be most concerned about inflation-proofing, so let’s focus on them.

Housing

The best way to inflation proof your housing expense it to own your residence. By having a mortgage, you lock in a fixed monthly housing cost that is not exposed to rent increases that may come with inflation. Having a completely paid-off home is even better as you completely remove the largest item in your budget. Preferably, this home is in a state with low property taxes as well.

When it comes to your mortgage, you have the option of a 15 year or 30 year mortgage. While the 15 year mortgage usually offers a better interest rate, so you pay less over the course of the loan, the 30 year mortgage offers more flexibility. If you have a 30 year mortgage and want to pay it off sooner, you can increase the amount of your monthly payments.

Owning real estate is perhaps the best hedge against inflation, as your fixed mortgage payment (which is typically your largest monthly expense) gets relatively cheaper as inflation increases the price of all assets.

Healthcare

Investing in your health

Ultimately, prioritizing your health and taking good care of yourself is the most important thing you can do to inflation-proof your healthcare costs. Your health is the single most important asset that you have. It is the foundation upon which you build everything else in your life. Without your health, nothing else matters. Treat your health just like you would treat your investments or your relationships: invest in it for the long term. Here are a few simple, inexpensive ways to invest in your health:

- Eat a healthy diet of high quality whole foods.

- Get lots of exercise, both cardio and strength training.

- Commit to getting proper sleep.

- Drink lots of water.

- Get adequate amounts of sunlight each day.

Affordable Care Act (ACA) Subsidies

After housing, healthcare is the other key area to consider when planning for early retirement. Assuming you wish to quit your job (thus losing your employer-sponsored health insurance), you will need to purchase your own health insurance until you are eligible for Medicare at age 65. This can be daunting, because private health insurance costs for middle aged people in the USA can be quite expensive. Finding affordable health insurance is possibly the biggest challenge to retiring early.

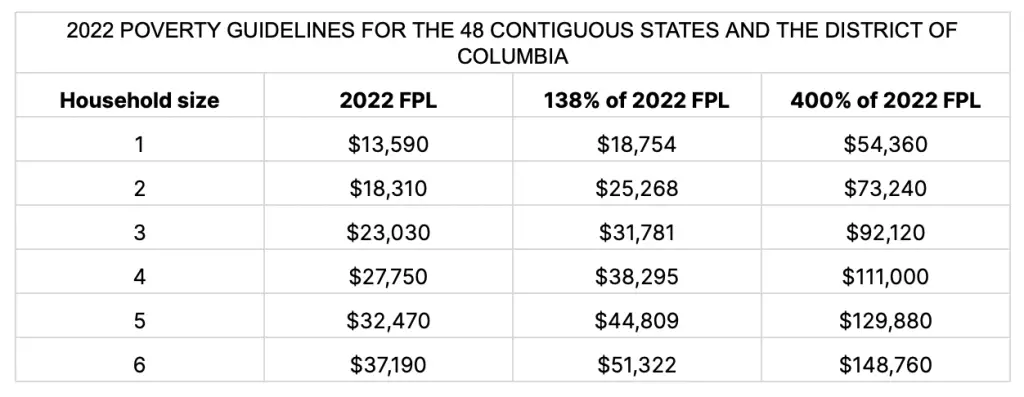

Fortunately, the Affordable Care Act (ACA), also known as ObamaCare, can be very helpful to early retirees looking to keep health insurance costs under control. The ACA health insurance premiums are made affordable by a subsidy that comes in the form of a tax credit which is based on your income relative to the Federal Poverty Level (FPL), also known as the HHS Poverty guidelines. To qualify for any subsidy in 2023 and beyond, your household’s modified adjusted gross income (MAGI) must be at or below 4x the FPL. If your MAGI exceeds 400% of the FPL, even by one dollar, then you do not qualify for any subsidies. The table below shows how the FPL increases with household size.

The American Rescue Act made a temporary change to this policy in 2021 and 2022, turning the 400% FPL cliff into a gradual slope. This allows individuals to qualify for a premium subsidy even if their income exceeds 400% of FPL, however your subsidy decreases as your income goes up.

There is also a minimum income required to get accepted by the ACA marketplace which depends on the state you live in. In Medicaid expansion states, if you make below 138% of the FPL, then you qualify for Medicaid, which provides extremely low cost health insurance premiums. However in non-Medicaid expansions states, Medicaid eligibility is not based on income, so if you make below the FPL and do not otherwise qualify for Medicaid, then you are neither eligible for Medicaid or eligible for ACA subsidies. KFF provides a great map that tracks the status of non-Medicaid expansion states.

The folks at KFF made an excellent interactive calculator to check the price of your health insurance premium under the ACA based on your household’s income, size, and age.

What the ACA means for early retirees

If we are thinking about the ACA through the lens of early retirees, let’s assume that you are no longer saving, so your MAGI is equal to your annual expenses.

For early retirement folks, the key to taking advantage of the ACA is to keep your MAGI below the 400% FPL number in order to qualify for subsidies. And the lower your MAGI, the greater your subsidy. Let’s look at an example of a household of 2 people, both age 35 years old, in early retirement with an income of $40,000 per year. According to the KFF calculator, they would qualify for subsidies worth $8,772 per year, which is a substantial chunk of their annual budget that they would otherwise have to pay!

The subsidy is large enough that if your MAGI is near the 400% FPL cliff, then it is worth keeping your income below the cliff value so that you still qualify for the subsidy. Let’s look at an example of a household of 2 people, both age 35 years old, with an income right at $73,000 (4x the FPL). If they keep their income just below the 400% FPL level, they would still qualify for subsidies worth about $4,000 per year. They would have to make over $77,000 per year to break even compared to keeping their income below 4x the FPL.

The easiest way to keep your annual expenses low without sacrificing quality of life is having a paid-off mortgage, which goes back to our previous point about inflation-proofing your housing expense. With your largest line item eliminated from your monthly expenses, you can keep your MAGI lower and qualify for greater premium subsidies.

Since the FPL is a fixed national average, living in a higher cost-of-living (COL) area does not change your FPL cliff, meaning that your higher annual expenses push you to the same cliff much faster. Thus, moving to a lower COL area where you have lower annual expenses keeps you further from the cliff and allows you to qualify for greater subsidies.

If you are on the ultra-lean early retirement wagon, then living in a state that has medicaid expansion will enable you to get extremely low cost health insurance premiums if you can keep your annual expenses below 138% of FPL.

Medical Tourism

For more internationally-minded (early) retirees, another option to keep healthcare costs low is moving to or traveling to another country that has cheaper but still high quality health care, also known as medical tourism. Other countries often have dramatically lower out-of-pocket costs for procedures and medications that can make it well worth the trip. Common categories of procedures that medical tourists pursue include dental care, cosmetic, and non-cosmetic surgery. Popular destinations for medical tourism include Mexico and central America as well as southeast Asian countries.

Education

If you’re retiring early and have children, there is a possibility that you will want to support the costs of their college education after you retire early. The cost of college tuition has grown much faster than inflation over the last few decades, so this is definitely an area to consider in your plan.

In the US, you and your child provide your financial details through the Free Application for Federal Student Aid (FAFSA) which then determines your custom cost of college. The FAFSA uses your financial situation to determine federal grants, work-study, and loans that you are eligible for. All the colleges that you are accepted to then use your FAFSA to determine your custom cost of college.

Your income is the largest factor that the FAFSA uses to calculate your custom cost of college. This income can include things like capital gains, dividend income, rental income, and even IRA conversions in a Roth ladder. In FAFSA’s eyes, your assets are divided between “protected” assets including your primary residence, HSAs, and your retirement accounts, and “unprotected” assets which are all of your other assets like cash, brokerage accounts, and investment properties. The FAFSA ignores your protected assets but expects parents to use up to 5.6% of your protected assets towards the cost of college.

To maximize your child’s financial aid as an early retiree, you want to minimize your income and push as much of your assets in to the protected category as possible. Once again, owning your home outright is a practical strategy because it lowers the income you need to draw from investments and also moves more of your assets into the protected category.

Aside from optimizing for the FAFSA, there are many ways to keep college costs under control. I wrote here about how I graduated college with no student loans and over $40k in savings without ever applying for the FAFSA.

College is only expensive if you make it expensive. Here are some other strategies for keeping college affordable:

- Attend a lower-cost community college and then transfer to a state school after two years.

- Attend a military service academy.

- Apply for merit-based scholarships.

- Take advantage of employer tuition reimbursement.

- Encourage your child to go into a skilled trade, where they will be getting paid to learn.

Investments

Now that we’ve covered your expenses, what about inflation-proofing your investments? This is pretty simple: just follow the timeless strategy of investing in low-cost index funds. Inflation tends to cause companies to raise their prices, which in turn leads to elevated revenues, earnings, and stock prices. Historically, the S&P500 has trended upward since its inception even after adjusting for inflation. This is the basis for the infamous 4% rule based on the Trinity study that is prevalent in the FIRE community.

Next to stocks, real estate is the other main inflation-proof pillar of investing. Owning your primary residence allows you to lock in your largest monthly expense with a fixed interest rate mortgage, so even as inflation increases the cost of housing around you, your monthly housing cost is fixed. Rental properties are also great hedges against inflation because again, your costs are fixed while your rental income grows as inflation increases rents.