Overview: should you use I-Bonds for your emergency fund?

The short answer is yes, you should! I-bonds are a fantastic pillar of your savings plan as they earn you a high risk-free return on your idle cash and protect you from inflation.

If you’re just starting out with buying I-bonds, you should keep at least some of your emergency fund in a fully liquid account (like a savings, checking, or money market account) since you are required to wait 12 months to cash out your I-bond after you purchase it.

A great strategy is to setup an I-bond ladder which moves your emergency fund into I-Bonds over time rather than all at once, allowing you to keep your emergency fund accessible while also earning the high interest I-Bonds provide. Whether you buy a lump sum of I-Bonds or setup an I-Bond ladder depends on the size of your emergency fund and your income stability.

What are I-bonds?

With US inflation hitting a 40-year high in 2022, Series I Savings Bonds, also known as I-Bonds, have recently surged in popularity due to their high risk-free yield which is based on current inflation. The interest rate for I-Bonds is set at 6.89% effective through April 30, 2023. This makes them a very attractive place to park your cash as this yield is essentially risk-free.

I-Bonds are safe investments issued by the U.S. Department of the Treasury (US Treasury) designed to protect your money from losing value due to inflation. I-Bonds offer an essentially risk-free return since they are backed by the full faith and credit of the US federal government and their redemption value cannot decline.

The interest you earn on an I-Bond is calculated using a composite rate which includes both a fixed interest rate and a variable interest rate which changes with inflation. Every 6 months, an updated composite rate is set by the U.S. Treasury to reflect current inflation. Interest is earned monthly, and compounded semiannually. This means that every 6 months, the interest rate is applied to a new principal which is the sum of the previous principal plus all interest accrued over the previous 6 months.

What are important things to know about I-bonds?

Before you start using I-Bonds as part of your savings and emergency fund strategy, there are a few key I-Bond requirements you should know.

Annual Purchase Limit

Purchases of electronic I-Bonds are limited to $10,000 per one Social Security Number or one Employer Identification Number each calendar year. You can purchase up to $10,000 in I-Bonds for each member of your household, however each I-Bond purchase must be made using each individual’s Social Security Number. You can also purchase up to $10,000 for each business you have, including sole proprietorships.

1 Year Initial Lock-up Period

A key thing to understand about buying I-Bonds is that each I-Bond you purchase can only be redeemed after you have held it for one year after the date of purchase.

This means that you should not put money into an I-Bond that you will need within the next year. Keep this in mind if you are thinking about using I-Bonds as part of your emergency fund strategy. The I-Bond Ladder strategy covered in the next section helps to address this lock-up period.

5 Year Period to Withdraw Full Interest Earnings

You are also required to hold the I-Bond for 5 years after the purchase date to earn the full interest. If you redeem your I-bond in less than 5 years of holding (but after 1 year), then you lose the last 3 months of interest that has accrued. Don’t let this deter you from I-Bonds however, because even if you lose the last 3 months of interest, I-Bonds still offer far better risk-free interest than any alternatives. After you’ve held the I-Bond for 5 years, you can redeem it with no penalty to your interest.

Using the I-Bond Ladder Strategy for your Emergency Fund

Emergency Fund Considerations

Now that you’re aware of the requirements for holding I-Bonds, let’s take a look at how you can use I-Bonds as a part of your emergency fund strategy.

Zooming out, an emergency fund is a cash reserve that you set aside to cover unexpected expenses or emergencies. Having money set aside for surprises helps you to get through short-term emergencies without going into debt and jeopardizing yourself long-term. Some examples include losing a job, car or home repairs, or medical bills.

It is generally recommended that you keep a minimum of 3 to 6 months worth of living expenses in your emergency fund, but a good goal is to have 12 months or more of runway saved up. The peace of mind that comes with knowing you could go without a job for an entire year is a huge relief from the day-to-day stress of life. You can use my Emergency Fund Calculator to calculate and visualize your personal emergency fund.

How much runway you should stash away depends on your personal situation, including how stable and in-demand your job is, your debts, and any other safety nets that you may have.

The I-Bond Ladder Strategy Explained with Examples

Since your I-Bonds are locked up for 1 year after you purchase them, a clever approach you can use to start buying I-Bonds while also keeping your emergency fund accessible (liquid) is what I call the I-Bond ladder. With this strategy, instead of buying $10,000 in I-Bonds all at once, you setup a recurring monthly purchase of I-Bonds, so you slowly move your money from your liquid account to I-Bonds. Each monthly I-Bond purchase then starts its own 1 year countdown to when you are able to redeem it.

This means that until your first I-Bonds start to clear the one year lockup period, your accessible Emergency Fund will be reduced by a maximum of $10,000. So the larger your emergency fund, the less impact that transitioning to I-Bonds has on your accessible Emergency Fund cash.

Let’s look at an example of using the I-Bond ladder strategy to understand why it makes more sense as you increase the size of your emergency fund.

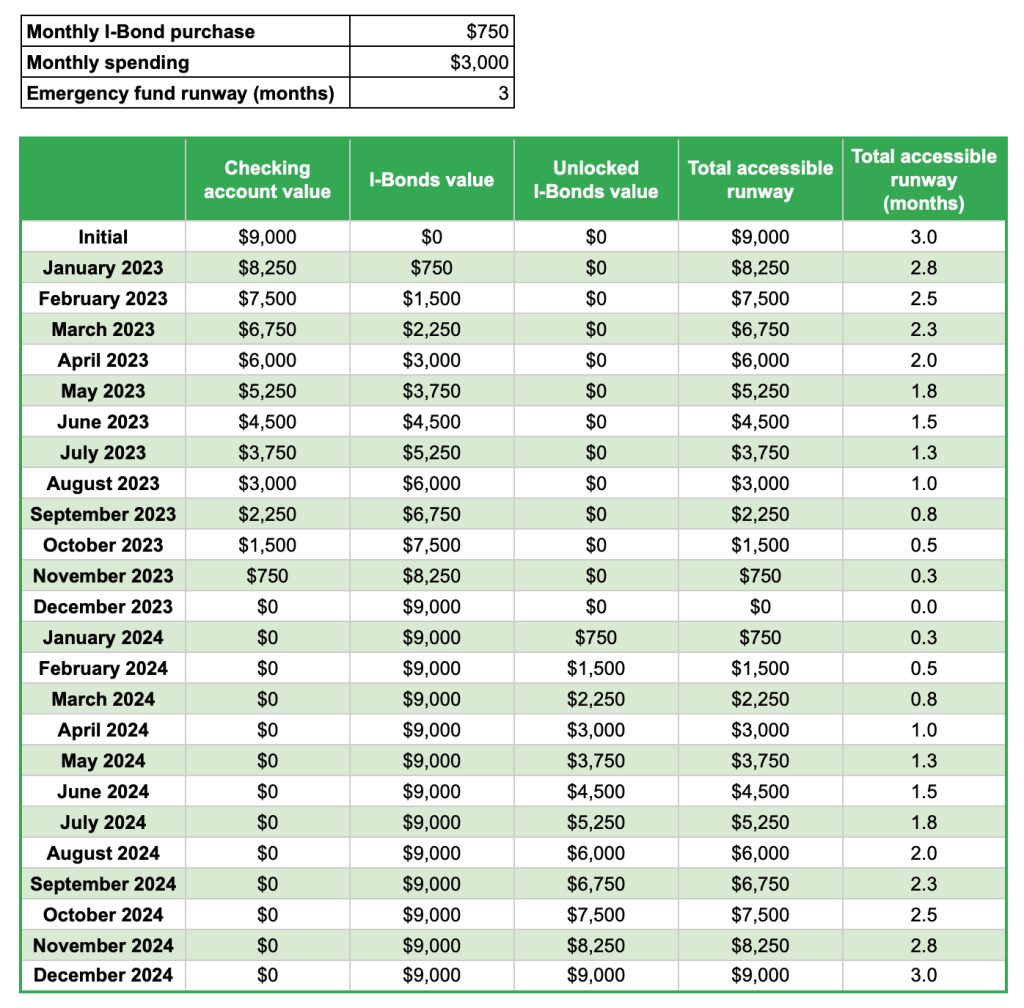

Scenario 1

Andrew spends $3,000 per month and has 3 months of runway in his emergency fund. If he moves $750 from his cash account into I-Bonds each month starting in January, we can see that his available runway goes down to $0 by the end of the first year, and then climbs back up to $9,000 by the end of the second year once all the I-Bonds become redeemable. This is dangerous because his Emergency Fund becomes very inaccessible during the transition.

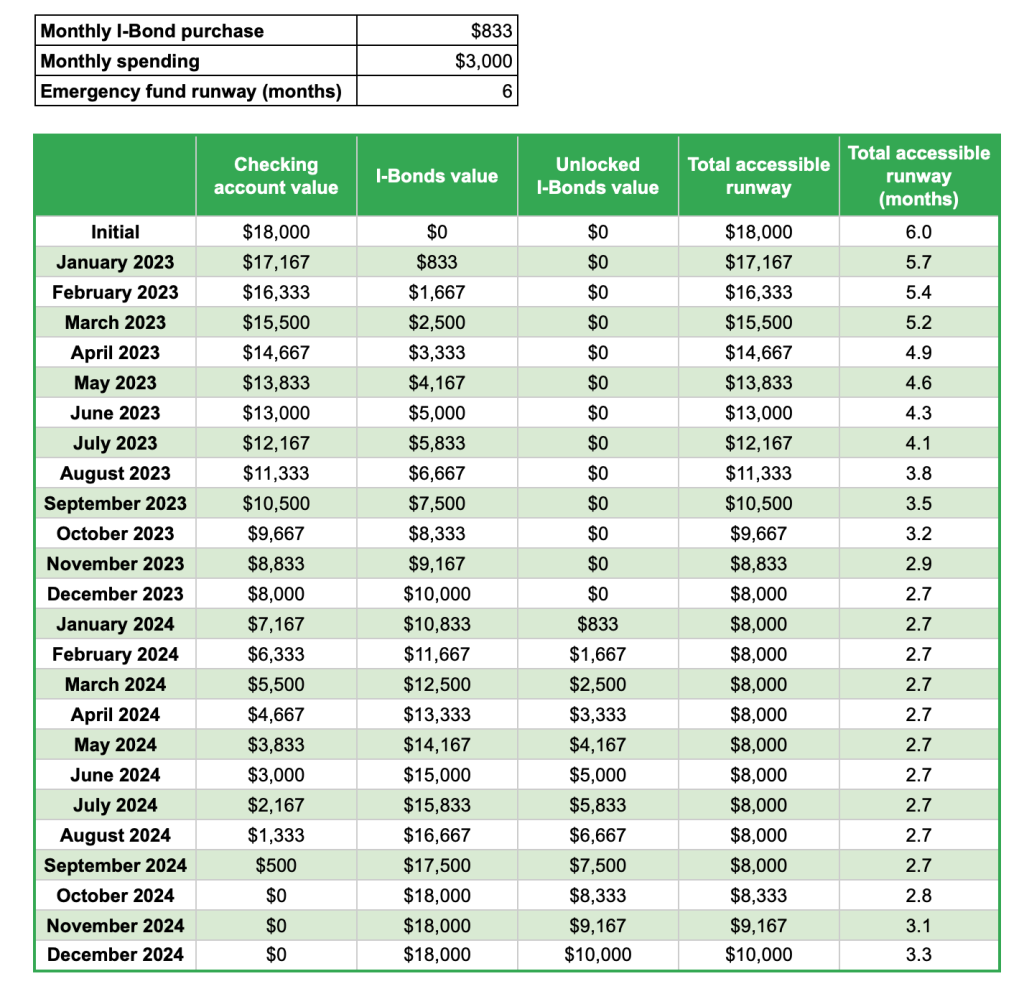

Scenario 2

Andrew spends $3,000 per month and has 6 months of runway in his emergency fund. If he moves $833 from his cash account into I-Bonds each month starting in January, we can see that his available runway goes down to 3 months by the end of the first year, and then hovers at 3 months through the end of the second year as his Emergency Fund continues to move into I-Bonds. It won’t be until the end of the third year that the full 6 months of runway is fully available. This is a bit more manageable.

Remember that if you do need to tap into your Emergency Fund while doing the I-Bond ladder, you can simply pause your I-Bond purchases to keep more runway on hand.

How to buy I-bonds

To purchase I-Bonds, you will first need to setup an account at TreasuryDirect.gov. TreasuryDirect is the U.S. Department of the Treasury’s platform for buying securities like I-Bonds and Treasury Bills directly from the U.S. government.

During the account setup process, you will need to provide personal information, including:

- Tax ID Number (SSN or EIN)

- E-mail Address

- Bank Account and Routing Number to fund your TreasuryDirect account

TreasuryDirect makes it difficult to change your bank account after the initial setup, so be sure to link a bank account that you plan to use for a long time when you setup your account.

Once you go through the steps and submit your application, your account will get processed and you will receive an email from TREASURY.DIRECT@fiscal.treasury.gov with your account number. At this stage, the email from TreasuryDirect may ask you to complete an account authorization form and mail it to their PO Box in order for you to open your account. This is somewhat common and the form is fairly quick to fill out, however you will need to obtain a seal or stamp from a notary or a financial institution.

Once you mail in the form, you should get an email about two weeks later stating that your hold has been lifted and you can access your account.

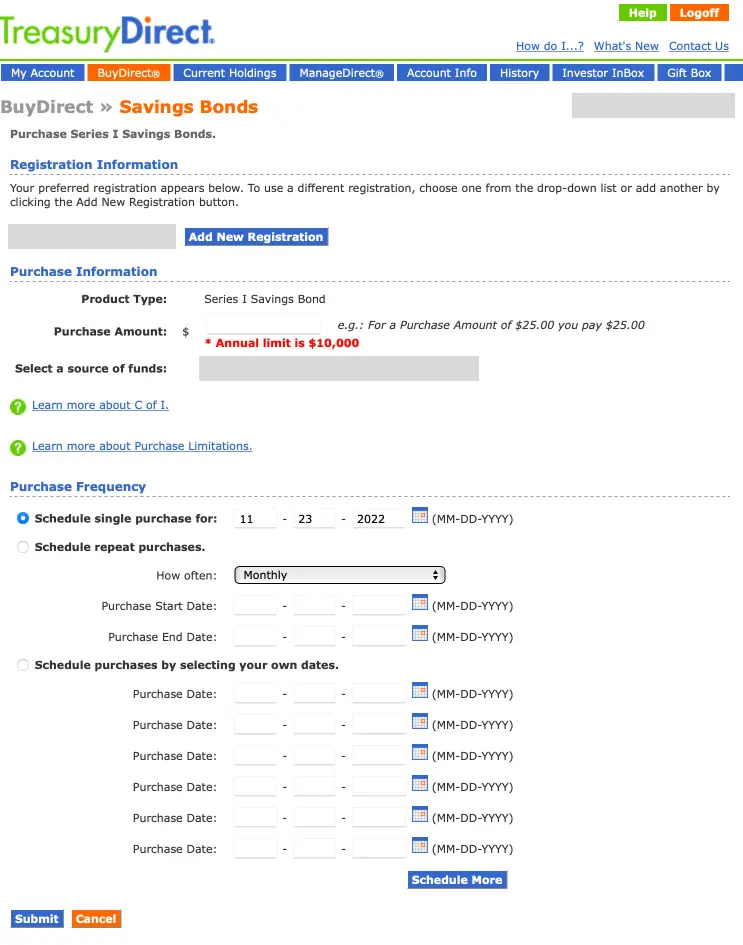

To setup your recurring I-Bonds purchase, first login and then click on the BuyDirect tab.

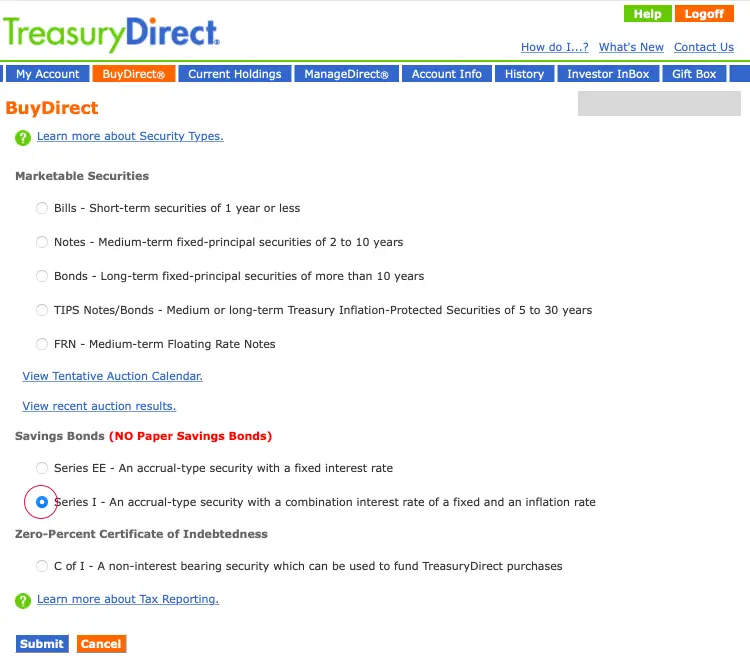

Choose Savings Bonds > Series I from the list and hit Submit.

In the Purchase Frequency section, you can setup a single purchase or repeat purchases. For repeat purchases, you can schedule the frequency of recurring purchases with a start and end date, or you can preselect individual purchase dates. Hit Submit and you are all set!